A rare opportunity to maximise your State Pension amount ends soon

This article was written by Antony Summers and originally published by Canaccord Wealth.

For some, the UK State Pension is a key part of their retirement income, while others rely on additional income streams. Whether it forms a significant portion or just one element of your broader retirement plan, the full entitlement can make a significant difference to your long-term financial wellbeing.

Currently, to qualify for the full State Pension entitlement, you need 35 years of National Insurance (NI) contributions. If you haven’t reached this threshold - you have until your State Pension age to do so - you may not receive the full amount.

Fortunately, there’s a unique, time-limited opportunity to top up your State Penson with voluntary NI contributions. If this opportunity could be right for you, our independent Wealth Planners will be able to offer you guidance and explore how you can make the most of it.

There are several reasons why some people have gaps in their NI contributions: early retirement, maternity or paternity leave, extended time out of work to raise a family or work abroad. If this applies to you, you may be able to ‘buy back’ missing years and increase your State Pension.

How many years of National Insurance can I buy back?

Normally, you can buy back up to six years, but when the 'new' State Pension was introduced in 2016, transitional arrangements allowed you to fill gaps as far back as 2006.

Originally set to end in April 2023, this window has now been extended until 5 April 2025 due to high demand.

How do I check if I’m missing NI contributions?

Before making any decisions, it’s important to check whether you have gaps in your contributions. You can do this easily online with the UK government’s NI record tool, through your personal tax account, or on the official HMRC app. You can also view your State Pension forecast to understand how much you’re currently on track to receive in the future.

If you do find out you’re missing NI contributions and are unlikely to naturally fill the gaps and receive the full entitlement, you may need to then consider if buying back years will benefit you and your personal circumstances. However, paying for gaps doesn’t guarantee you will receive more pension: eligibility depends on your individual circumstances.

Is it worth me buying back years – even if I’m a higher rate taxpayer?

Before making any decision, you should assess whether this opportunity makes financial sense for you. It’s not a one-size-fits-all solution. That’s why we would suggest speaking with a Wealth Planner to look at your personal situation.

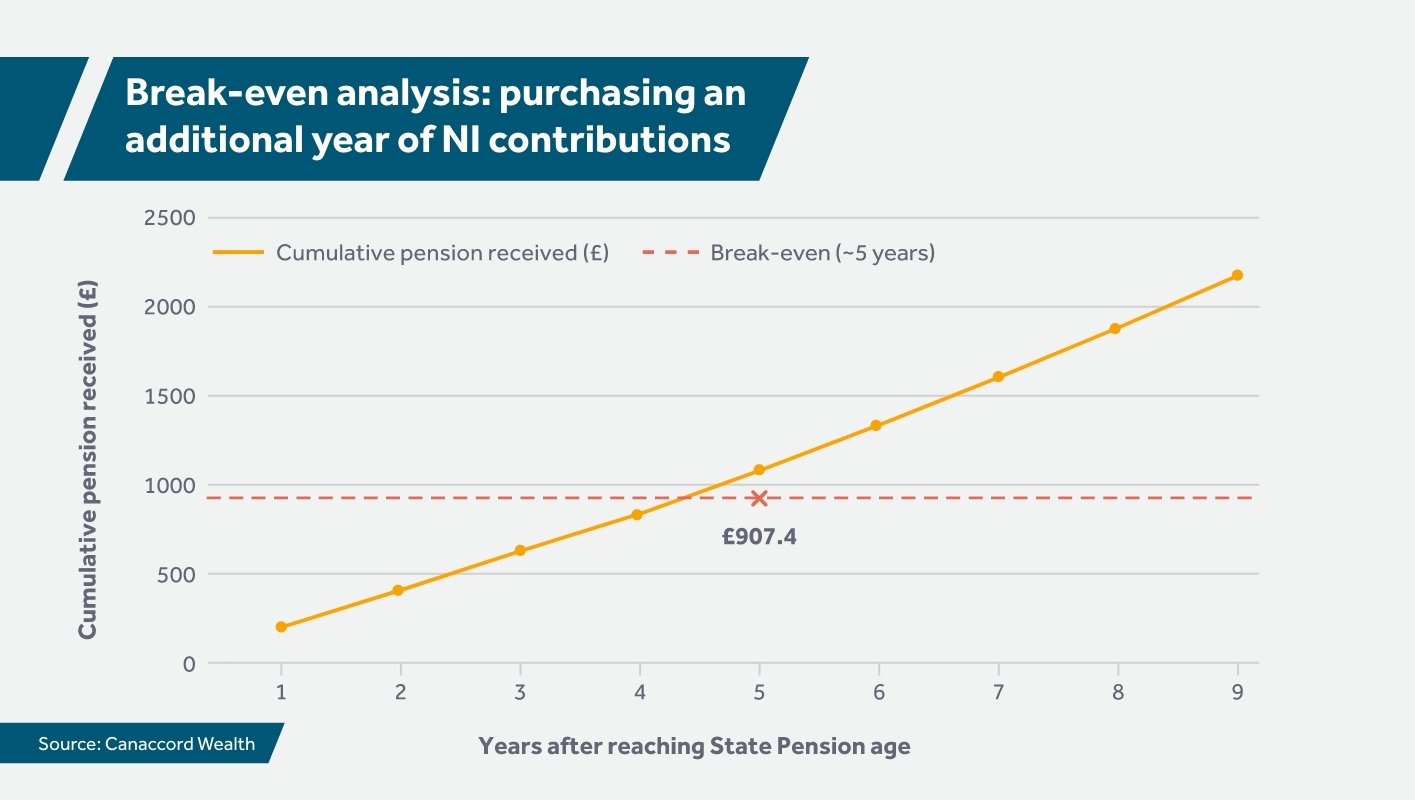

For those already in retirement, the ‘break-even point’ - when the extra pension received outweighs the cost of the voluntary contributions - can come sooner than for someone still working.

For example, purchasing an additional year of contributions costs £907.40 for the 2024–25 tax year. As the graph below shows, a higher-rate taxpayer in retirement could recoup this cost in around five years, assuming a 5% annual State Pension increase.

Political risks and future changes

While the current rules present a significant opportunity for some, it’s important to remember that pension laws can change. Future governments may adjust eligibility criteria, entitlement levels, or contribution rules, which could impact whether buying back years is worthwhile.

Although it’s unlikely the State Pension will be abolished, legislative changes could mean this opportunity won’t be as beneficial later on. That’s why it’s important to assess your position now while the current rules apply.

As mentioned earlier, it all depends on your personal circumstances – something that a no-obligation initial conversation with our Wealth Planners will consider.

How do I pay voluntary NI contributions to HMRC?

If you find that you have gaps and agree with your Wealth Planner that it’s worthwhile to top up, consider the method of how you’ll fund the extra contributions. A first step could be to speak to the Future Pension Centre to understand the specifics of how to make payments. You might choose to pay via direct debit or other arrangements such as online or telephone or even by cheque to HMRC.

You can visit the UK government website and find more details on paying Class 2 or Class 3 voluntary contributions (depending if you’re self-employed or not).

With the 5 April 2025 deadline approaching, now is the time to review your State Pension entitlement and take action if needed. To explore your options, visit GOV.UK before speaking with an independent Wealth Planner.

Adam and Company’s independent Wealth Planners offer expert retirement planning, from reviewing your pension arrangements to investing for the future and beyond. Get in touch with us for a free initial no-obligation consultation.

You may also be interested in:

- Post-budget webinar: Our experts unlock the pension puzzle

- Navigating the UK Budget: your wealth planning priorities and next steps

- The secrets of calculating a wealthy retirement

Need more help?

Whatever your needs, we can help by putting you in contact with the best expert to suit you.

Investment involves risk. The value of investments and the income from them can go down as well as up and you may not get back the amount originally invested. The information provided is not to be treated as specific advice. It has no regard for the specific investment objectives, financial situation or needs of any specific person or entity. The tax benefits depend upon the investor’s individual circumstances and clients should discuss their financial arrangements with own tax adviser before investing. The levels and bases of taxation may be subject to change in the future.

Find this information useful? Share it with others...

Antony Summers

Antony, a Wealth Planning Director, provides investment and financial planning advice to private clients, trusts, pension schemes, and charities. With expertise in investment consultancy for individuals, trusts, and charities, he combines significant financial planning experience with a strong tax background from his time at an accountancy firm.

A proponent of Life Planning, Antony helps clients assess and achieve their long-term financial goals. He is a Certified Financial Planner, qualified in investment management through the UK Society of Investment Professionals, and a member of the Personal Finance Society and the Chartered Insurance Institute.

0207 523 4609

Investment involves risk and you may not get back what you invest. It’s not suitable for everyone.

Investment involves risk and is not suitable for everyone.